Date and Time Calculators

( 1 )Date and Time Calculators – Accurate Tools for Everyday Use Welcome to our collection of…

Learn more

Type a tool name, a problem, or a trust page topic and pick from live suggestions as you go.

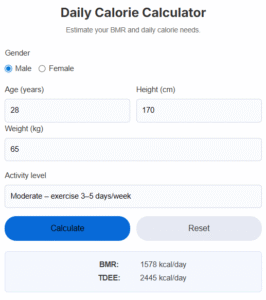

Quick answer: A calorie calculator gives you a useful starting estimate, but daily calorie needs are best adjusted using real…

Quick answer: A car insurance estimator is best for comparison shopping, not for choosing a policy on price alone. This…

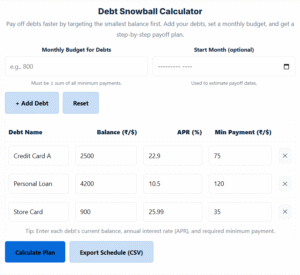

What this guide adds beyond the calculator The debt snowball calculator shows the numbers, but the method also depends on…

⚡ Quick answer: Standard adult BMI ranges (kg/m²) are: under 18.5 underweight, 18.5-24.9 healthy, 25-29.9 overweight, 30+ obese. These ranges apply to ages 20-65 of both sexes, but children, teens, older adults, and athletes need adjusted interpretation. Use a BMI Calculator to find your value, then check the right reference range for your age.

Body Mass Index (BMI) is the most widely used screening tool for healthy weight worldwide — but it is not a one-size-fits-all measure. Your age, sex, body composition, and ethnic background all influence how to interpret your number. This guide walks through the standard ranges and where they need adjustment.

BMI is calculated as weight in kilograms divided by height in metres squared (kg/m²). It estimates total body weight relative to height, not body fat directly. The formula was developed in the 19th century by Belgian statistician Adolphe Quetelet as a population measure — not an individual diagnostic.

Modern medicine uses BMI as a quick screening tool: a value in the healthy range usually means low metabolic risk; a high or low value warrants closer examination by a doctor.

These ranges are based on the World Health Organization classification and apply to adults aged 20-65 regardless of sex. The WHO does note that for some Asian populations, the overweight threshold is lower (23) and obesity threshold is 27.5 — reflecting different metabolic risk profiles at lower BMIs.

The WHO ranges are not sex-adjusted. However, women typically have higher body-fat percentage at the same BMI than men, while men carry more muscle mass. Two practical implications:

For under-20s, the standard adult ranges do NOT apply. Instead, doctors use BMI-for-age percentiles from the CDC or WHO growth charts:

Adolescents go through growth spurts. A BMI that jumps a category in one year can simply reflect normal development. Always interpret a child”s BMI with a pediatrician.

For older adults, recent research suggests a slightly higher “healthy” BMI range — typically 23-30 — is associated with the lowest mortality risk. Underweight in older adults often signals frailty, malnutrition, or underlying disease. Aim for stable weight rather than aggressive weight loss after 65 unless a doctor advises otherwise.

BMI is a useful population-level screening tool but a rough individual measure. For most people in the middle of the range, it correlates well with health risk; at the edges it can mislead, especially for muscular individuals or older adults.

The numerical ranges are the same. However, the same BMI represents a higher body-fat percentage in women on average. Pair BMI with body-composition or waist measurement for a fuller picture.

For ages 20-65 the standard 18.5-24.9 range applies. Children use age-specific percentiles. Adults over 65 may have a healthier range of 23-30 according to recent mortality studies.

Muscle is denser than fat. A muscular athlete weighing 95 kg at 180 cm tall has a BMI of 29.3 (“overweight”) but very low body-fat. BMI cannot distinguish muscle from fat.

The WHO recognises adjusted cut-offs for some Asian populations: overweight at 23 and obesity at 27.5. This reflects higher metabolic risk at lower BMIs in these groups.

A BMI of 25-27 with no other risk factors and healthy waist measurement is generally not concerning. Above 27, talk to a healthcare provider — especially if combined with high blood pressure, blood sugar, or family history.

Every 6-12 months for healthy adults. More often if actively managing weight. Children should be checked at well-visits using percentile charts.

Waist circumference, waist-to-hip ratio, body-fat percentage (via DEXA, BIA scale, or skinfold callipers), and metabolic markers (blood pressure, lipid panel, glucose). The best assessments combine multiple measurements.